The example of a typical dairy farmer whose income has halved this year illustrates how the "bad year" tax break option introduced by Minister for Finance Michael Noonan can help.

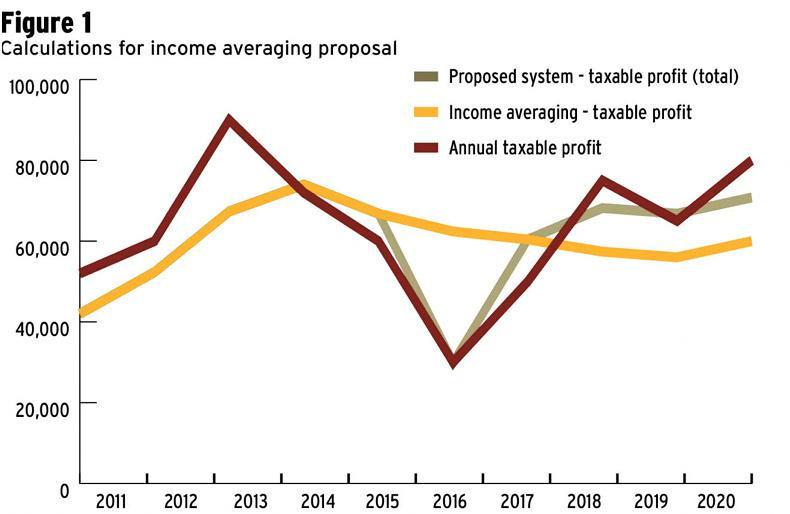

The figure above shows how the new income averaging rules will work.

The example is for a dairy farmer with about 100 cows and no debt or capital investments needed.

The red line shows taxable profit each year. Profit falls in 2016 to €30,000, about half the average of other years.

ADVERTISEMENT

The yellow line shows taxable profit if the farmer is using the current income averaging rules.

The rules put his 2016 taxable

income at €62,400, which would

result in a high tax bill in a difficult year.

The grey line shows taxable profit each year using the opt-out allowed for this year under the new rules introduced in Budget 2017. Taxable profit in 2016 is €30,000. That reduces the tax bill to be paid for this year.

We can see that the deferred taxable income is added in three equal shares to taxable income made in 2018, 2019 and 2020. Higher tax would arise in those years.

The total amount of tax paid over the five years remains the same – one of the basic points of income averaging.

In summary:

In the above graph, the red line shows actual taxable income arising each year before use of income averaging. Note the drop in income in 2016.

The yellow line shows taxable income under the current averaging rules – note how taxable income is deemed not to have fallen significantly in 2016. Instead, taxable income falls in the following years (2016-2020), as the effect of 2016 feeds through.

Finally, the grey line shows how the new opt-out rule allows a farmer to declare a lower taxable income in 2016. We see how the deferred taxable income appears in the years 2017 to 2020, with higher tax bills than arising in those years.

This content is available to digital subscribers and loyalty code users only. Sign in to your account, use the code or subscribe to get unlimited access.

However, if you would like to share the information in this article, you may use the headline, summary and link below:

Title: Budget 2017: income averaging case study

The example of a typical dairy farmer whose income has halved this year illustrates how the "bad year" tax break option introduced by Minister for Finance Michael Noonan can help.

The reader loyalty code gives you full access to the site from when you enter it until the following Wednesday at 9pm. Find your unique code on the back page of Irish Country Living every week.

CODE ACCEPTED

You have full access to the site until next Wednesday at 9pm.

CODE NOT VALID

Please try again or contact support.

The figure above shows how the new income averaging rules will work.

The example is for a dairy farmer with about 100 cows and no debt or capital investments needed.

The red line shows taxable profit each year. Profit falls in 2016 to €30,000, about half the average of other years.

The yellow line shows taxable profit if the farmer is using the current income averaging rules.

The rules put his 2016 taxable

income at €62,400, which would

result in a high tax bill in a difficult year.

The grey line shows taxable profit each year using the opt-out allowed for this year under the new rules introduced in Budget 2017. Taxable profit in 2016 is €30,000. That reduces the tax bill to be paid for this year.

We can see that the deferred taxable income is added in three equal shares to taxable income made in 2018, 2019 and 2020. Higher tax would arise in those years.

The total amount of tax paid over the five years remains the same – one of the basic points of income averaging.

In summary:

In the above graph, the red line shows actual taxable income arising each year before use of income averaging. Note the drop in income in 2016.

The yellow line shows taxable income under the current averaging rules – note how taxable income is deemed not to have fallen significantly in 2016. Instead, taxable income falls in the following years (2016-2020), as the effect of 2016 feeds through.

Finally, the grey line shows how the new opt-out rule allows a farmer to declare a lower taxable income in 2016. We see how the deferred taxable income appears in the years 2017 to 2020, with higher tax bills than arising in those years.

If you would like to speak to a member of our team, please call us on 01-4199525.

Link sent to your email address

We have sent an email to your address. Please click on the link in this email to reset your password. If you can't find it in your inbox, please check your spam folder. If you can't find the email, please call us on 01-4199525.

ENTER YOUR LOYALTY CODE:

The reader loyalty code gives you full access to the site from when you enter it until the following Wednesday at 9pm. Find your unique code on the back page of Irish Country Living every week.

SHARING OPTIONS