This is a subscriber-only article

This is a subscriber-only article

All the milk processors held their milk prices for November. Some processors introduce winter milk supply bonuses in November, but these are not included in the monthly league as they are conditional bonuses and not all supply is getting the bonus allocated.

The volumes collected by processors in south falls off dramatically in November and December. November volumes (this league price) represents about 4% of annual supply for the typical supplier, with December falling to 2%. While volumes are up slightly this autumn compared with last year, they are still small in the context of the annual supply.

Along the whole of the west coast, December milk supply is up over 20% compared with the same period last year.

Arrabawn reports early December figures up over 20%, Drinagh up 20%, Aurivo up 18%, while Kerry Group is up over 35%.

Aurivo was the only company to reduce October milk price but has held for November and so remains in the mix at the top.

West Cork

The west Cork co-ops remain in division one and they have a November 0.88c/litre milk quality bonus (for milk under 200 cells/ml SCC). Arrabawn and Lakeland are the other two processors in division one for November.

On average, the price paid for November milk was €4.81/kg milk solids or 34.35c/l ex-VAT at 3.3% protein and 3.6% fat. In effect, this means that November milk is achieving a very good price when you take into account the seasonal milk solids and the very good milk price.

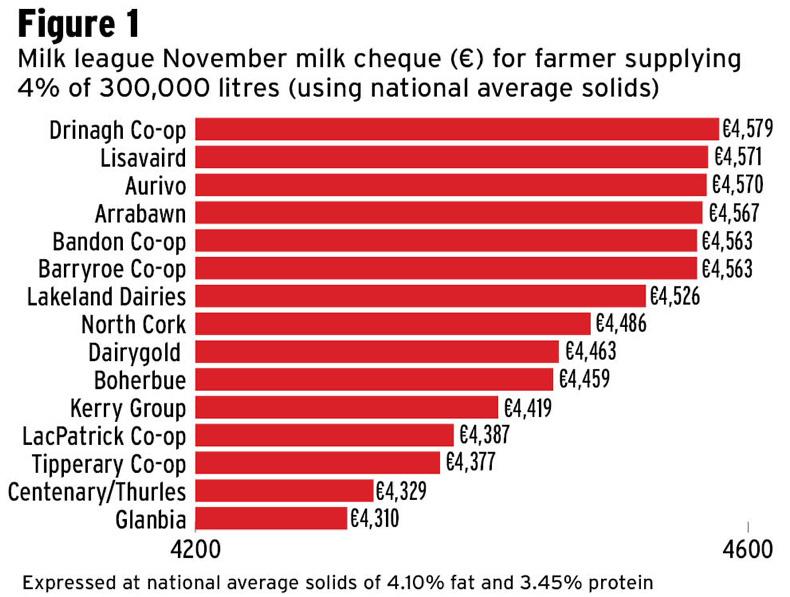

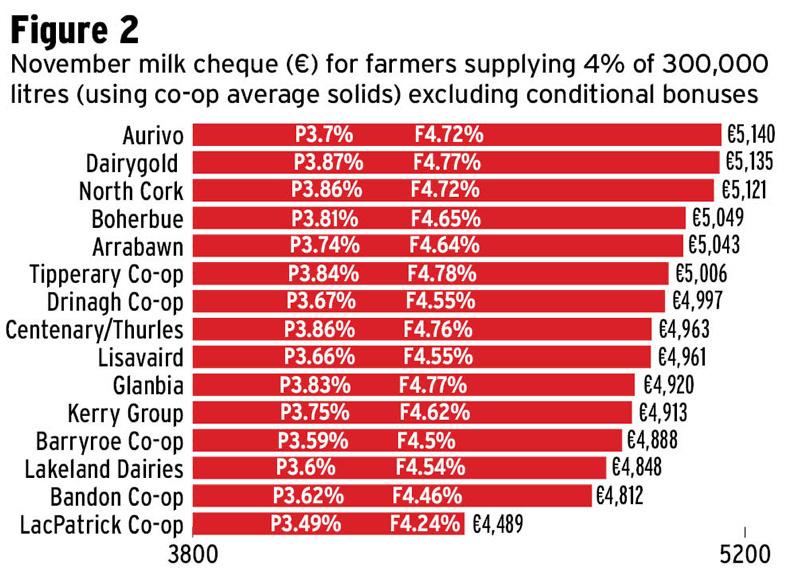

Figure 1 and Figure 2 show the November milk cheque for each processor using the national average solids (4.10% fat and 3.45% protein) and the co-op solids for the month respectively. As you can see, there is a gap of €268 in the November milk cheque for Drinagh compared with Glanbia.

End-of-year bonus

While an Ornua bonus is more than likely in the pipeline (for early spring 2018), Carbery has unexpectedly already announced (following the last board meeting) that it would pay an end-of-year bonus of 1c/l on all 2017 milk supplies.

IFA chair Sean O’Leary was quick out of the blocks to welcome that announcement and said all dairy co-ops should be able to follow that example given the excellent trading year in 2017. Sean suggests that the average gap between the price paid by co-ops and the returns from the EU marker was around 2c/l.

SHARING OPTIONS: