The price decreases that set in after the summer of 2014 continued until mid-2016. The upturn since then was too late to prevent the average milk price paid by EU dairy companies falling by €2.77 (8.9%) to €28.30 per 100kg in 2016 in comparison with 2015. This made 2016 the second-worst milk price year since 1999. The only year the milk price was lower was 2009.

Besides the low milk prices, 2016 was also memorable for the big differences in monthly price observed. Monthly milk prices bottomed out at the start of the summer and increased strongly again at the end of the year.

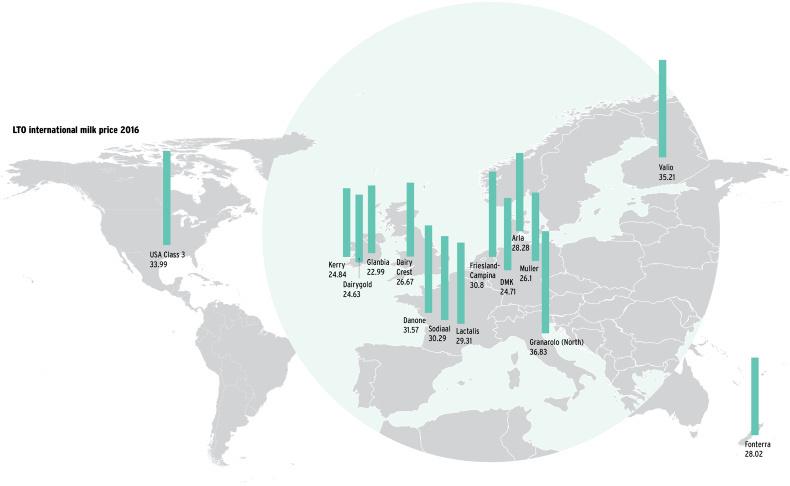

International milk price comparison allows a dairy farmer to compare what dairy farmers are getting paid in one country with another. The prices listed in Table 1 show the LTO price comparison for 15 dairy companies operating across the world. It’s fair to say it reflects a price where the large pools of milk are produced but within that there are differences between companies depending on product mix and export or internal trade.

In general, milk prices in Italy and Finland are well above the average applicable in the rest of the European Union. One possible explanation for Italy could be the relative scarcity of farm milk. Italy is a net importer of dairy and much of the raw milk available is used to make special types of high-value cheese (Parmesan and Grana Padano, for example). Similar to other high-priced companies, Granarolo uses a large volume of milk to make fresh dairy products.

As Finland is a net dairy exporter, this reasoning does not explain the high milk price paid by Valio, but the Finnish milk pool is declining and retains a high cost of production.

As we have covered previously numerous times, Valio does produce a relatively large number of innovative products with high added value. What is striking is the high ranking of Danone and the other French companies.

It would seem that French milk prices rank relatively higher in poor milk price years, but farmers supplying French processors have other challenges and costs as they effectively are still ruled by limits on what you can supply.

The figures

The LTO International Milk Price Comparison is published every month at the request of the dairy committee of the Dutch Federation of Agriculture and Horticulture (LTO Nederland). It is a comparison of prices paid for milk by large European companies and is done in co-operation with European Dairy Farmers (EDF). EDF collects the milk price data and makes it available. Calculations are undertaken by ZuivelNL.

The method chosen for the calculations shows the price a dairy farmer would receive if milk of specific (standard) composition, quality and quantity were delivered to the different dairy companies.

In this report the following characteristics of the standard milk are taken as a basis:

The prices are exclusive of VAT, ex-farm and inclusive of supplementary payments.

It must be emphasised that this is not a comparison of the average milk prices paid. The average price paid by a dairy company for milk is dependent on the actual composition, quality, etc of the milk delivered. Furthermore, no conclusions can be drawn about the performance of dairy companies on the basis of the milk prices paid alone. Many more factors play a role in assessing overall performance.

Comparison details

France

The French milk price system is set out in contracts between producer organisations and the milk buyers. The volume of milk that dairy farms are able to supply each year is restricted. If milk is supplied over and above the limit applicable, milk farmers receive a very low price for this so-called surplus milk. The French system is similar to the old milk quota system, but different in that the quota is now determined at milk buyer’s level and the superlevy previously charged for extra milk has been replaced by a very low milk price, which has the same effect.

The French milk price consists of a base price for standard milk, plus or minus various bonuses and/or deductions, depending on actual fat and protein content and quality, etc. The base price is derived from the average base price applicable in the previous year, plus a monthly adjustment (indexation) based on market indicators published by CNIEL. Also, to keep in step with competitors to some extent, allowance is made for the difference between French and German milk prices.

Because the sale of dairy products in the French domestic market (less fluctuation) affects the market indicators relatively more than the export of basic products to third countries, which fluctuates in price far more, price fluctuations are reduced compared with other countries.

New Zealand

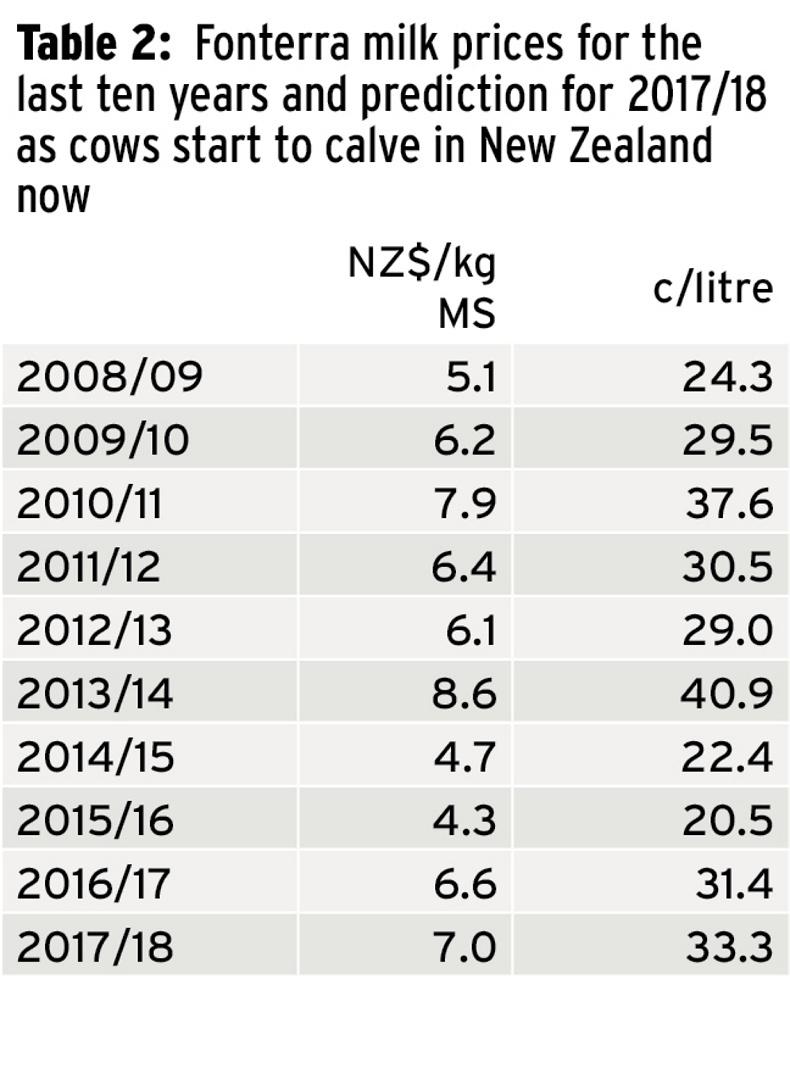

The Fonterra dairy co-operative processes approximately 84% of all farm milk in New Zealand and 95% of New Zealand’s dairy production is exported. With this in mind, the development in the milk prices paid by Fonterra is a good indication of the prices applicable in the global dairy market.

Given the limited amount of competition, the farm gate milk price of Fonterra is determined on the basis of a transparent government-backed methodology. The New Zealand milk price is expressed per kg of fat and protein (milk solids (MS)).

Fonterra publishes a milk price forecast at the start of each milk price season. This forecast is updated on a regular basis throughout the milk price season, which runs from June to May inclusive. The final milk price is announced once the financial year has ended in September.

The milk price forecasts show the turnaround in the dairy market, with a 41% increase in the milk price forecast between 1 August and 18 November 2017.

Throughout the season, the calculated milk price is based on the most recent forecast, plus the dividend expected. The latter is taken into consideration because members are required to buy one share per kg of MS.

The member-dairy farmers receive a monthly advance milk price in accordance with a predetermined schedule, which is derived from the milk price forecast and takes cashflow at farm level into consideration. As such, the advance milk price is different to the amounts specified in the table.

The milk price calculated for Fonterra for calendar year 2016 is €28.02 (2015: €21.05) per 100kg. This is based on the final milk price of NZ$4.30 per kg MS (including a dividend of NZ$0.40) in the 2015/16 season and the most recent forecast for the current 2016/17 season, being NZ$6.65 (including a dividend of NZ$0.50).

Fonterra has announced an opening milk price of NZ$6.50 per kg MS with effect from June 2017 for the new 2017/2018 season. Including an estimated dividend of NZ$0.50, this corresponds with a milk price including dividend of NZ$7.00 per kg MS.

The milk price for the previous season and the forecast for 2017/18 are far higher than the price for the last two milk price seasons (see Table 2).

The US

The Class III milk price gives a good indication of how milk prices are developing in the US. The government (USDA) publishes monthly prices for different classes of raw milk, depending on the destination of the milk – Class IV (butter and skimmed milk powder), Class III (cheese), Class II (other processed milk) and Class I (consumption milk and consumption milk products). The prices of the underlying components (fat and protein, etc) are published also. These prices are based on extensive market observations.

The milk prices paid to milk farmers are largely determined by the milk processor’s product folio and, with this in mind, a weighted average of the various class prices. Besides the destination of the milk, prices vary depending on market regulation per state, cost deductions by the buyers and/or bonuses paid and, of course, actual content and quality.

Because Class III is regarded as the most representative, this is the starting point taken when calculating the US milk price.

Milk prices are converted into an amount per 100kg of standard milk, based on the corresponding prices of underlying components.

Ireland

Kerry

The calculated milk price of Kerry includes a sustainability bonus of 0.1c/l.

Dairygold

The milk prices paid by the Irish Dairygold co-operative have been included in the milk price comparison since January 2015. According to the annual report, an amount of €25m was paid out in milk price support in 2016. Based on 1.2bn kg of milk, this equates to some €2.00 per 100kg. Support amounted to approximately €1.70 per 100kg in 2015.

Glanbia Ingredients Ireland

The milk price calculated by Glanbia Ingredients Ireland (GII) excludes payments received from the support fund of the Glanbia co-operative (an average of €1.35 in 2016 and €1.15 per 100kg in 2015). These co-op bonuses have not been included in the milk price calculated, being a payment from the capital of the co-operative and, as such, not linked to the market returns achieved by Glanbia Ingredients. The co-operative owns 31% of all shares in the listed company Glanbia plc and receives a dividend on an annual basis. GII is a joint venture of the co-operative and Glanbia plc.

Ornua’s payment of 1c/l has also not been included either. Ornua (previously the Irish Dairy Board) is a co-operative that exports the dairy products of its Irish member-dairy companies to international markets.

All profits made are channelled back (in part) to the member co-operatives, which – as is the case with Glanbia – are then able to pass on an amount to the dairy farmers.

Milk Price review – focus on Fonterra

Milk price review – focus on Arla

Milk Review – focus on FrieslandCampina

Milk review – focus on Dairy Farmers of America

Milk Price review – focus on Valio